"Markets change and so will we." TM

COMPLIMENTARY HIDDEN FEE ANALYSIS

Uncover Hidden Fees in Your Investments

Maximize Your Wealth by Understanding the True Cost of Your Portfolio

At Lily Wealth Management, we believe in full transparency. Many investors unknowingly pay excessive fees that impact long-term growth. Our Hidden Fees Analysis service helps you uncover these costs and make informed decisions about your financial future.

WHAT WE ANALYZE

ETF Costs in Your Portfolio

-

Provide us a recent statement and we’ll run a KWANTI Analytics Report to uncover hidden ETF fees. You may be shocked!

Variable Annuities Cost Breakdown

-

Click here to see some examples on how your annuity stacks up against major providers like Allianz, Allstate, John Hancock, Lincoln, New York Life, Prudential, and Hartford.

-

For a free cost comparison fill out the form below

High-Cost Sub-Account Fees in Variable Annuities

-

Many annuities have higher expense sub-account fees that erode returns. We help you identify and reduce these costs.

-

Understand how most expenses are deducted before you even see your returns.

Fixed & Equity-Indexed Annuity Cost Breakdown

-

With insurance-based products, compounding occurs annually, reducing long-term gains.

-

In your portfolio, compounding occurs daily—maximizing growth.

-

Some annuities offer only a 1% guaranteed minimum on 87% of your deposit, not 100% of your deposit. Therefore you only have a .87% guarantee, not 1%.

Exposing the Hidden Fees That Others Won't Tell you About in Variable Annuities

M&E Fees

For Example: Suppose you invest $200,000 in a variable annuity.

The annuity contract charges an M&E fee of 1.25% annually (which is fairly typical — the range is often 0.90%–1.50% per year).

This fee compensates the insurance company for providing the death benefit, the guarantee of lifetime income options, and administrative costs.

So:

Annual M&E charge = $200,000 × 1.25% = $2,500

This $2,500 is deducted from your account value over the year, usually in daily or monthly increments.

A Real Example: Hidden Fees in a Variable Annuity

Before the TD-Schwab merger, we helped a client transition from a Mass Mutual Group Variable Annuity to a TD Ameritrade account.

What we uncovered in the process was — quite frankly — one of the most egregious examples of hidden fees we’ve seen in over 30 years in the industry.

Here’s what the client was paying in subaccount fees inside their annuity compared to what they paid when they moved their money from Mass Mutual to TD Ameritrade:

The difference was staggering — thousands of dollars annually being quietly siphoned away through excessive fees.

In our opinion, this situation was a disgrace — to the industry, to the 401(k) space, and to the hard-working investors it hurt.

Three parties share responsibility:

-

The insurance company — for charging such egregious fees.

-

The mutual fund companies — for cutting hidden deals behind closed doors.

-

The regulators — for looking the other way and allowing minimal disclosures.

We even filed a formal complaint with the Department of Labor because, as we say:

“Big print giveth, small print taketh away.”

This experience motivates us every day to fight for transparency and fairness on behalf of our clients.

Hidden Fees Matter

In variable annuities Admin fees and M&E fees come out on a daily basis off the top of performance and you never see it. Here are three prime examples below (taken from Jefferson National/Nationwide website), assuming $200,000 with a 6% return over 20 years. Sometimes there are additional sub-account management fees added on that the insurance company receives, like a kickback.

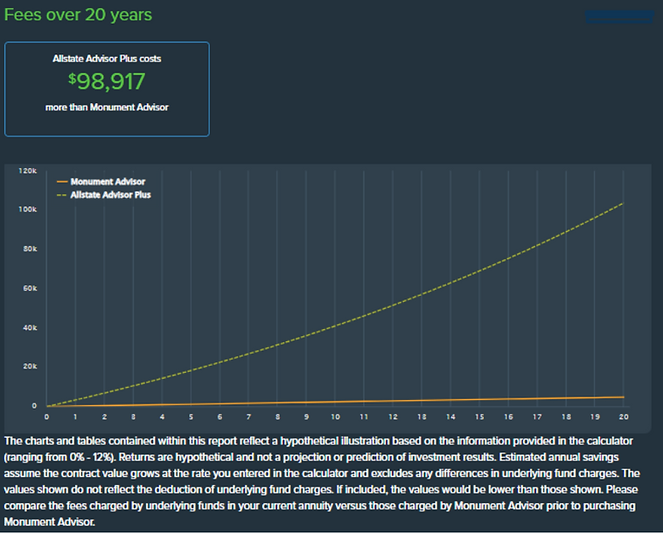

Allstate Hidden Fees

For illustrative purposes only

Fees can be called many things in fixed equity indexed annuities

Spreads - A fee that reduces your return

For Example:

Let’s say your annuity is linked to the S&P 500 Index, and the annuity uses a 3% spread.

-

If the S&P 500 gains 10% in a year, your credited return would be:

-

10% – 3% spread = 7% credited to your annuity.

-

-

If the index gains 2%, your return would be:

-

2% – 3% spread = 0% (You don’t lose money, but you earn nothing that year.)

-

-

If the index is negative, you typically earn 0%, not a loss (thanks to the FIA’s principal protection feature).